Recent days I got curious that what topics attract most of economists' attentions. NBER working paper series contain some relatively new research fruits so I used it as the raw input.

It is not hard to extract key words from these papers' titles. After that, I made a further step that matched all single keys to academic keywords on Microsoft Academic.

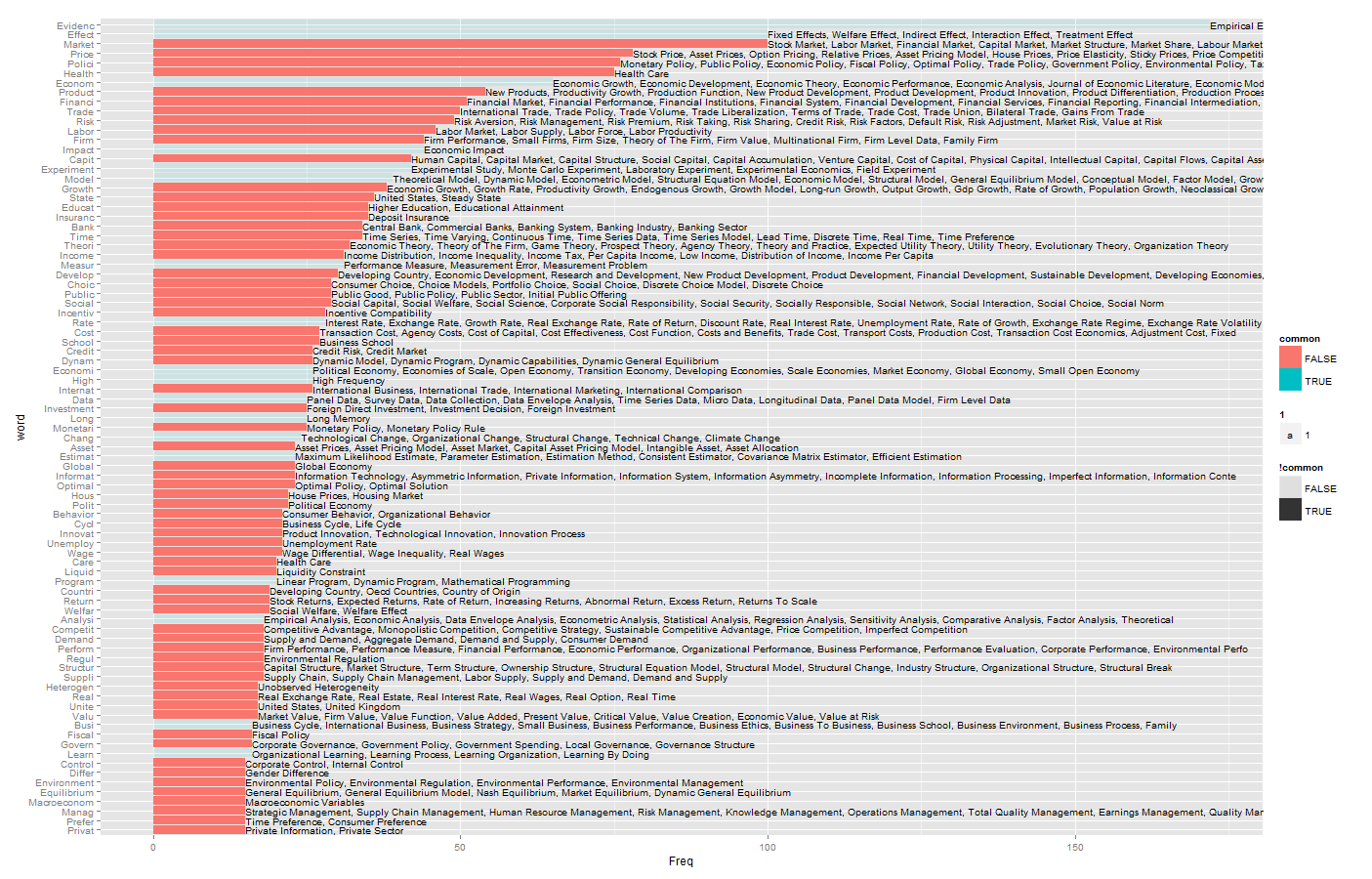

From a glance, I manage to identify some hot keys:

Price. Health. Social. Policy/Public. Risk/asset/liquidity. Growth. Insurance. Education/School.

For reproducible purpose, my code is here.

grab_url <- c("http://www.nber.org/new_archive/mar14.html",

"http://www.nber.org/new_archive/dec13.html",

"http://www.nber.org/new_archive/sep13.html",

"http://www.nber.org/new_archive/jun13.html",

"http://www.nber.org/new_archive/mar13.html")

library(RCurl)

require(XML)

grab_paper <- function (grab) {

webpage <- getURLContent(grab)

web_content <- htmlParse(webpage,asText = TRUE)

paper_title <- sapply(getNodeSet(web_content, path="//li/a[1]"),xmlValue)

author <- sapply(getNodeSet(web_content, path="//li/text()[1]") ,xmlValue)

paper_author <- data.frame(paper_title = paper_title, author = author)

return(paper_author)

}

library(plyr)

paper_all <- ldply(grab_url,grab_paper)

titles <- strsplit(as.character(paper_all$paper_title),split="[[:space:]|[:punct:]]")

titles <- unlist(titles)

library(tm)

library(SnowballC)

titles_short <- wordStem(titles)

Freq2 <- data.frame(table(titles_short))

Freq2 <- arrange(Freq2, desc(Freq))

Freq2 <- Freq2[nchar(as.character(Freq2$titles_short))>3,]

Freq2 <- subset(Freq2, !titles_short %in% stopwords("SMART"))

Freq2$word <- reorder(Freq2$titles_short,X = nrow(Freq2) - 1:nrow(Freq2))

Freq2$common <- Freq2$word %in% c("Evidenc","Effect","Econom","Impact","Experiment","Model","Measur","Rate","Economi",

"High","Data","Long","Chang","Great","Estimat","Outcom","Program","Analysi","Busi"

,"Learn","More","What")

library(ggplot2)

ggplot(Freq2[1:100,])+geom_bar(aes(x=word,y=Freq,fill = common,alpha=!common))+coord_flip()

### get some keywords from Bing academic

start_id_Set = (0:5)*100+1

require(RCurl)

require(XML)

# start_id =1

#

get_keywords_table <- function (start_id) {

end_id = start_id+100-1

keyword_url <- paste0("http://academic.research.microsoft.com/RankList?entitytype=8&topDomainID=7&subDomainID=0&last=0&start=",start_id,"&end=",end_id)

keyword_page <- getURLContent(keyword_url)

keyword_page <- htmlParse(keyword_page,asText = TRUE)

keyword_table <- getNodeSet(keyword_page, path="id('ctl00_MainContent_divRankList')//table")

table_df <- readHTMLTable(keyword_table[[1]])

names(table_df) <- c("rowid","Keywords" , "Publications" ,"Citations")

return (table_df)

}

require(plyr)

keywords_set <- ldply(start_id_Set,get_keywords_table)

save(keywords_set, file="keywords_set.rdata")